2018 540 Forms and Instructions Personal Income Tax Booklet

Important Dates

When the due date falls on a weekend or holiday, the deadline to file and pay without penalty is extended to the next business day.

| April 15, 2019* | Last day to file and pay the 2018 amount you owe to avoid penalties and interest.* See form FTB 3519 for more information. * If you are living or traveling outside the United States on April 15, 2019, the dates for filing your tax return and paying your tax are different. See form FTB 3519 for more information. |

|---|---|

| October 15, 2019 | Last day to file or e-file your 2018 tax return to avoid a late filing penalty and interest computed from the original due date of April 15, 2019. |

| April 15, 2019 June 17, 2019 September 16, 2019 January 15, 2020 |

The dates for 2019 estimated tax payments. Generally, you do not have to make estimated tax payments if your California withholding in each payment period totals 90% of your required annual payment. Also, you do not have to make estimated tax payments if you will pay enough through withholding to keep the amount you owe with your tax return under $500 ($250 if married/registered domestic partner (RDP) filing separately). However, if you do not pay enough tax either through withholding or by making estimated tax payments, you may have an underpayment penalty. See Form 540-ES instructions for more information. |

$$$ for You

Earned Income Tax Credit

- Federal Earned Income Tax Credit (EIC) – EIC reduces your federal tax obligation, or allows a refund if no federal tax is due. You may qualify if you earned less than $49,194 ($54,884 if married filing jointly) and have qualifying children or you have no qualifying children and you earned less than $15,270 ($20,950 if married filing jointly). Call the Internal Revenue Service (IRS) at 800-829-4477 and when instructed enter topic 601, see the federal income tax booklet, or go to the IRS website at irs.gov and search for eitc assistant.

- California Earned Income Tax Credit (EITC) – EITC reduces your California tax obligation, or allows a refund if no California tax is due. You may qualify if you have wage income earned in California and/or net earnings from self-employment of less than $24,951. You do not need a child to qualify. For more information go to ftb.ca.gov and search for EITC or get form FTB 3514 – California Earned Income Tax Credit.

Refund of Excess State Disability Insurance (SDI)

If you worked for at least two employers during 2018 who together paid you more than $114,967 in wages, you may qualify for a refund of excess SDI. See the instructions on page 14.

Common Errors and How to Prevent Them

Help us process your tax return quickly and accurately. When we find an error, it requires us to stop to verify the information on the tax return, which slows processing. The most common errors consist of:

- Claiming the wrong amount of estimated tax payments.

- Claiming the wrong amount of standard deduction or itemized deductions.

- Claiming a dependent already claimed on another return.

- The amount of refund or payments made on an original return does not match our records when amending your tax return.

- Claiming the wrong amount of withholding by incorrectly totaling or transferring the amounts from your W-2.

- Claiming the wrong amount of real estate withholding.

- Claiming the wrong amount of SDI.

- Claiming the wrong amount of exemption credits.

To avoid errors and help process your tax return faster, use these helpful hints when preparing your tax return.

Claiming estimated tax payments:

- Verify the amount of estimated tax payments claimed on your tax return matches what you sent to the Franchise Tax Board (FTB) for that year. Go to ftb.ca.gov and login or register for MyFTB to view your total estimated tax payments before you file your tax return.

- Verify the overpayment amount from your 2017 tax return you requested to be applied to your 2018 estimated tax.

Claiming state disability insurance:

- Verify the amount of SDI used to figure the amount of excess SDI claimed on Form 540, line 74, matches amounts from your W-2’s.

Claiming standard deduction or itemized deductions:

- See Form 540, line 18 instructions and worksheets for the amount of standard deduction or itemized deductions you can claim.

Claiming withholding amounts:

- Go to ftb.ca.gov and login or register for MyFTB to verify withheld amount or see instructions for line 71 of Form 540 or line 81 of Form 540NR. Confirm only California income tax withheld is claimed.

- Verify real estate or other withholding amount from Form 592-B, Resident and Nonresident Withholding Statement, and Form 593, Real Estate Withholding Tax Statement. See instructions for line 73 of Form 540 or line 83 for Form 540NR.

Claiming refund or payments made on an original return when amending your tax return:

- Go to ftb.ca.gov and login or register for MyFTB to check tax return records for refund or payments made.

- Verify the amount from your original return line 115 of Form 540 or line 125 of Form 540NR and include any adjustment by FTB.

Use e-file:

- By using e-file, you can eliminate many common errors. Go to ftb.ca.gov and search for efile options.

Do I Have to File?

Steps to Determine Filing Requirement

Step 1: Is your gross income (all income received from all sources in the form of money, goods, property, and services that are not exempt from tax) more than the amount shown in the California Gross Income chart below for your filing status, age, and number of dependents? If yes, you have a filing requirement. If no, go to Step 2.

Step 2: Is your adjusted gross income (federal adjusted gross income from all sources reduced or increased by all California income adjustments) more than the amount shown in the California Adjusted Gross Income chart below for your filing status, age, and number of dependents? If yes, you have a filing requirement. If no, go to Step 3.

Step 3: If your income is less than the amounts on the chart you may still have a filing requirement. See “Requirements for Children with Investment Income” and “Other Situations When You Must File.” Do those instructions apply to you? If yes, you have a filing requirement. If no, go to Step 4.

Step 4: Are you married/RDP filing separately with separate property income? If no, you do not have a filing requirement. If yes, prepare a tax return. If you owe tax, you have a filing requirement.

| On 12/31/18, my filing status was: | and on 12/31/18, my age was: (If your 65th birthday is on January 1, 2019, you are considered to be age 65 on December 31, 2018) | California Gross Income | California Adjusted Gross Income | ||||

|---|---|---|---|---|---|---|---|

| Dependents | Dependents | ||||||

| 0 | 1 | 2 or more | 0 | 1 | 2 or more | ||

| Single or Head of household |

Under 65 | 17,693 | 29,926 | 39,101 | 14,154 | 26,387 | 35,562 |

| 65 or older | 23,593 | 32,768 | 40,108 | 20,054 | 29,229 | 36,569 | |

| Married/RDP filing jointly Married/RDP filing separately (The income of both spouses/RDPs must be combined; both spouses/RDPs may be required to file a tax return even if only one spouse/RDP had income over the amounts listed.) |

Under 65 (both spouses/RDPs) | 35,388 | 47,621 | 56,796 | 28,312 | 40,545 | 49,720 |

| 65 or older (one spouse/RDP) | 41,288 | 50,463 | 57,803 | 34,212 | 43,387 | 50,727 | |

| 65 or older (both spouses/RDPs) | 47,188 | 56,363 | 63,703 | 40,112 | 49,287 | 56,627 | |

| Qualifying widow(er) | Under 65 | N/A | 29,926 | 39,101 | N/A | 26,387 | 35,562 |

| 65 or older | N/A | 32,768 | 40,108 | N/A | 29,229 | 36,569 | |

| Dependent of another person Any filing status |

Any age | More than your standard deduction (Use the California Standard Deduction Worksheet for Dependents on page 11 to figure your standard deduction.) | |||||

Requirements for Children with Investment Income

California law conforms to federal law which allows parents’ election to report a child’s interest and dividend income from children under age 19 or a student under age 24 on the parent’s tax return. For each child under age 19 or student under age 24 who received more than $2,100 of investment income in 2018, complete Form 540 and form FTB 3800, Tax Computation for Certain Children with Investment Income, to figure the tax on a separate Form 540 for your child.

If you qualify, you may elect to report your child’s income of $10,500 or less (but not less than $1,050) on your tax return by completing form FTB 3803, Parents’ Election to Report Child’s Interest and Dividends. To make this election, your child’s income must be only from interest and/or dividends. To get forms FTB 3800 or FTB 3803, see “Order Forms and Publications” or go to ftb.ca.gov/forms.

Other Situations When You Must File

If you have a tax liability for 2018 or owe any of the following taxes for 2018, you must file Form 540.

- Tax on a lump-sum distribution.

- Tax on a qualified retirement plan including an Individual Retirement Arrangement (IRA) or an Archer Medical Savings Account (MSA).

- Tax for children under age 19 or student under age 24 who have investment income greater than $2,100 (see paragraph above).

- Alternative minimum tax.

- Recapture taxes.

- Deferred tax on certain installment obligations.

- Tax on an accumulation distribution from a trust.

Filing Status

Use the same filing status for California that you used for your federal income tax return, unless you are a registered domestic partnership (RDP). If you are an RDP and file single for federal, you must file married/RDP filing jointly or married/RDP filing separately for California. If you are an RDP and file head of household for federal purposes, you may file head of household for California purposes only if you meet the requirements to be considered unmarried or considered not in a domestic partnership.

Exception: If you file a joint tax return for federal purposes, you may file separately for California if either spouse was:

- An active member of the United States armed forces or any auxiliary military branch during 2018.

- A nonresident for the entire year and had no income from California sources during 2018.

Community Property States: If the spouse earning the California source income is domiciled in a community property state, community income will be split equally between the spouses. Both spouses will have California source income and they will not qualify for the nonresident spouse exception.

If you had no federal filing requirement, use the same filing status for California that you would have used to file a federal income tax return.

If you filed a joint tax return and either you or your spouse/RDP was a nonresident for 2018, file the Long or Short Form 540NR, California Nonresident or Part-Year Resident Income Tax Return.

Single

You are single if any of the following was true on December 31, 2018:

- You were not married or an RDP.

- You were divorced under a final decree of divorce, legally separated under a final decree of legal separation, or terminated your registered domestic partnership.

- You were widowed before January 1, 2018, and did not remarry or enter into another registered domestic partnership in 2018.

Married/RDP Filing Jointly

You may file married/RDP filing jointly if any of the following is true:

- You were married or an RDP as of December 31, 2018, even if you did not live with your spouse/RDP at the end of 2018.

- Your spouse/RDP died in 2018 and you did not remarry or enter into another registered domestic partnership in 2018.

- Your spouse/RDP died in 2019 before you filed a 2018 tax return.

Married/RDP Filing Separately

- Community property rules apply to the division of income if you use the married/RDP filing separately status. For more information, get FTB Pub. 1031, Guidelines for Determining Resident Status, FTB Pub. 737, Tax Information for Registered Domestic Partners, or FTB Pub. 1032, Tax Information for Military Personnel. To get forms see “Order Forms and Publications” or go to ftb.ca.gov/forms.

- You cannot claim a personal exemption credit for your spouse/RDP even if your spouse/RDP had no income, is not filing a tax return, and is not claimed as a dependent on another person’s tax return.

- You may be able to file as head of household if your child lived with you and you lived apart from your spouse/RDP during the entire last six months of 2018.

Head of Household

For the specific requirements that must be met to qualify for head of household (HOH) filing status, get FTB Pub. 1540, California Head of Household Filing Status. In general, head of household filing status is for unmarried individuals and certain married individuals or RDPs living apart who provide a home for a specified relative. You may be entitled to use head of household filing status if all of the following apply:

- You were unmarried and not in a registered domestic partnership, or you met the requirements to be considered unmarried or considered not in a registered domestic partnership on December 31, 2018.

- You paid more than one-half the cost of keeping up your home for the year in 2018.

- For more than half the year, your home was the main home for you and one of the specified relatives who by law can qualify you for head of household filing status.

- You were not a nonresident alien at any time during the year.

For a child to qualify as your foster child for head of household purposes, the child must either be placed with you by an authorized placement agency or by order of a court.

California requires taxpayers who use head of household filing status to file form FTB 3532, Head of Household Filing Status Schedule to report how the HOH filing status was determined.

Beginning in tax year 2018, if you do not attach a completed form FTB 3532 to your tax return, we will deny your Head of Household filing status. For more information about the Head of Household filing requirements, go to ftb.ca.gov and search for HOH.

Qualifying Widow(er)

Check the box on Form 540, line 5 and use the joint return tax rates for 2018 if all five of the following apply:

- Your spouse/RDP died in 2016 or 2017 and you did not remarry or enter into another registered domestic partnership in 2018.

- You have a child, stepchild, or adopted child (not a foster child) whom you can claim as a dependent or could claim as a dependent except that, for 2018:

- The child had gross income of $4,150 or more;

- The child filed a joint return, or

- You could be claimed as a dependent on someone else’s return.

If the child isn’t claimed as your dependent, enter the child’s name in the entry space under the "Qualifying widow(er)" filing status.

- This child lived in your home for all of 2018. Temporary absences, such as for vacation or school, count as time lived in the home.

- You paid over half the cost of keeping up your home for this child.

- You could have filed a joint tax return with your spouse/RDP the year he or she died, even if you actually did not do so.

What’s New and Other Important Information for 2018

Differences between California and Federal Law

In general, for taxable years beginning on or after January 1, 2015, California law conforms to the Internal Revenue Code (IRC) as of January 1, 2015. However, there are continuing differences between California and federal law. When California conforms to federal tax law changes, we do not always adopt all of the changes made at the federal level. For more information, go to ftb.ca.gov and search for conformity. Additional information can be found in FTB Pub. 1001, Supplemental Guidelines to California Adjustments, the instructions for California Schedule CA (540), California Adjustments – Residents, and the Business Entity tax booklets.

The instructions provided with California tax forms are a summary of California tax law and are only intended to aid taxpayers in preparing their state income tax returns. We include information that is most useful to the greatest number of taxpayers in the limited space available. It is not possible to include all requirements of the California Revenue and Taxation Code (R&TC) in the instructions. Taxpayers should not consider the instructions as authoritative law.

Conformity

For updates regarding federal acts, go to ftb.ca.gov and search for conformity.

2018 Tax Law Changes/What’s New

Voluntary Contributions

You may contribute to the following new funds:

- Organ and Tissue Donor Registry Voluntary Tax Contribution Fund

- National Alliance on Mental Illness California Voluntary Tax Contribution Fund

- Schools Not Prisons Voluntary Tax Contribution Fund

Federal Tax Reform

The Tax Cuts and Jobs Act (TCJA) signed into law on December 22, 2017, made changes to the IRC. In general, California R&TC does not conform to the changes. California taxpayers continue to follow the IRC as of the specified date of January 1, 2015, with modifications. For specific adjustments due to the TCJA, see the Schedule CA (540) instructions.

California Earned Income Tax Credit (EITC)

For taxable years beginning on or after January 1, 2018, the age limit for an eligible individual without a qualifying child is revised to 18 years or older. For more information, go to ftb.ca.gov and search for EITC or get form FTB 3514, California Earned Income Tax Credit.

New Employment Credit

The sunset date for the New Employment Credit is extended until taxable years beginning before January 1, 2026. For more information, go to ftb.ca.gov and search for nec or get form FTB 3554, New Employment Credit.

California Competes Tax Credit

The sunset date for the California Competes Tax Credit is extended until taxable years beginning before January 1, 2030. For more information, go to the GO-Biz website at business.ca.gov or ftb.ca.gov and search for ca competes or get form FTB 3531, California Competes Tax Credit.

Native American Earned Income Exemption

For taxable years beginning on or after January 1, 2018, federally recognized tribal members living in California Indian country who earn income from any federally recognized California Indian country are exempt from California taxation. This exemption applies only to earned income. Enrolled tribal members who receive per capita income must reside in their affiliated tribe’s Indian country to qualify for tax exempt status. Additional information can be found in the instructions for Schedule CA (540) and form FTB 3504, Enrolled Tribal Member Certification.

Like-Kind Exchanges

The TCJA amended IRC Section 1031 limiting its application to real property that is not primarily held for sale. Additionally, under the TCJA, exchanges of personal property and intangible property do not qualify for nonrecognition of gain or loss as like-kind exchanges. California does not conform to the amendments under the TCJA. Get Schedule D-1, Sales of Business Property.

IRC Section 965 Deferred Foreign Income

Under federal law, if you own (directly or indirectly) certain foreign corporations, you may have to include on your return certain deferred foreign income. California does not conform. For more information, see the Schedule CA (540) instructions.

Global Intangible Low-Taxed Income (GILTI) Under IRC Section 951A

Under federal law, if you are a U.S. shareholder of a controlled foreign corporation, you must include your GILTI in your income. California does not conform. For more information, see the Schedule CA (540) instructions.

Other Important Information

Wrongful Incarceration Exclusion

California law conforms to federal law excluding from gross income certain amounts received by wrongfully incarcerated individuals for taxable years beginning before, on, or after January 1, 2018. If you included income for wrongful incarceration in a prior taxable year, you can file an amended California personal income tax return for that year. If the normal statute of limitations has expired, you must file a claim by January 1, 2019.

College Access Tax Credit

For taxable years beginning on and after January 1, 2017, and before January 1, 2023, the College Access Tax Credit (CATC) is available to entities awarded the credit from the California Educational Facilities Authority (CEFA). The credit is 50% of the amount contributed by the taxpayer for the taxable year to the College Access Tax Credit Fund. The amount of the credit is allocated and certified by the CEFA. For more information, go to the CEFA website at treasurer.ca.gov and search for catc.

Schedule X, California Explanation of Amended Return Changes

For taxable years beginning on or after January 1, 2017, use Schedule X to determine any additional amount you owe or refund due to you, and to provide reason(s) for amending your previously filed income tax return. For additional information, see “Instructions for Filing a 2018 Amended Return” on page 29.

Improper Withholding on Severance Paid to Veterans

The Combat‑Injured Veterans Tax Fairness Act of 2016 gives veterans who retired from the Armed Forces for medical reasons additional time to claim a refund if they had taxes improperly withheld from their severance pay. If you filed an amended return with the IRS on this issue, you have two years to file your amended California return.

New Donated Fresh Fruits or Vegetables Credit

For taxable years beginning on or after January 1, 2017 and before January 1, 2022, qualified taxpayers may claim the New Donated Fresh Fruits or Vegetables Credit. This tax credit is for donations of fresh fruits or vegetables made to California food banks. The amount of the tax credit is 15% of the qualified value of the donated item, based on weighted average wholesale price. The credit may be claimed only on a timely filed original return. However, any credit not used in the taxable year may be carried forward up to seven years. For more information, get form FTB 3814, New Donated Fresh Fruits or Vegetables Credit.

Low-Income Housing Credit Allocations to Partners

For partnerships owning projects that receive a preliminary reservation of the Low‑Income Housing Credit (LIHC) before January 1, 2020, the prior law exception that requires a partnership to allocate the credit among partners based upon the partnership agreement is re-enacted.

Sale of Credit

For projects that receive a preliminary reservation of the LIHC beginning on or after January 1, 2016, and before January 1, 2020, a taxpayer may make an irrevocable election in its application to the California Tax Credit Allocation Committee to sell all or any portion of the LIHC allowed to one or more unrelated parties for each taxable year in which the credit is allowed. An original purchaser is allowed a one-time resale of that credit to one or more unrelated parties. For more information, get form FTB 3521, Low-Income Housing Credit, or go to the California Tax Credit Allocation Committee website at treasurer.ca.gov/ctcac.

California Achieving a Better Life Experience (ABLE) Program

For taxable years beginning on or after January 1, 2016, the California Qualified ABLE Program was established and California generally conforms to the federal income tax treatment of ABLE accounts. This program was established to help blind or disabled U.S. residents save money in a tax-favored ABLE account to maintain health, independence, and quality of life. Additional information can be found in the instructions of form FTB 3805P, Additional Taxes on Qualified Plans (Including IRAs) and Other Tax-Favored Accounts.

New California Motion Picture and Television Production Credit

For taxable years beginning on or after January 1, 2016, a new California motion picture and television production credit will be allowed to a qualified taxpayer. The credit is allocated and certified by the California Film Commission (CFC). The qualified taxpayer can:

- Offset the credit against income tax liability.

- Sell the credit to an unrelated party (independent films only).

- Assign the credit to an affiliated corporation.

- Apply the credit against qualified sales and use taxes.

For more information, get form FTB 3541, California Motion Picture and Television Production Credit, form FTB 3551, Sale of Credit Attributable to an Independent Film, go to ftb.ca.gov and search for motion picture, or go to the CFC website at film.ca.gov and search for incentives.

Electronic Funds Withdrawal (EFW)

Make extension or estimated tax payments using tax preparation software. Check with your software provider to determine if they support EFW for extension or estimated tax payments.

Payments and Credits Applied to Use Tax

For taxable years beginning on or after January 1, 2015, if a taxpayer includes use tax on their personal income tax return, payments and credits will be applied to use tax first, then towards income tax, interest, and penalties. Additional information can be found in the instructions for California Form 540.

Dependent Social Security Number (SSN)

For taxable years beginning on or after January 1, 2015, taxpayers claiming an exemption credit must write each dependent’s SSN in the spaces provided within line 10 for the California Form 540 and California Form 540NR (Long and Short).

Financial Incentive for Seismic Improvement

For taxable years beginning on or after January 1, 2015, taxpayers can exclude from gross income any amount received as loan forgiveness, grant, credit, rebate, voucher, or other financial incentive issued by the California Residential Mitigation Program or the California Earthquake Authority to assist a residential property owner or occupant with expenses paid, or obligations incurred, for earthquake loss mitigation. Additional information can be found in the instructions for California Schedule CA (540 and 540NR).

Natural Heritage Preservation Credit

For qualified contributions made on or after January 1, 2015, the credit carryover period has been extended to 15 years or until exhausted, whichever occurs first. Any unused credits remaining before January 1, 2015, will remain subject to an eight-year carryover provision. In addition, the period for when a qualified contribution is made, for which a tax credit will be allowed, has been extended to June 30, 2020.

Disaster Losses

For taxable years beginning on or after January 1, 2014, and before January 1, 2024, taxpayers may deduct a disaster loss for any loss sustained in any city, county, or city and county in California that is proclaimed by the Governor to be in a state of emergency. For these Governor-only declared disasters, subsequent state legislation is not required to activate the disaster loss provisions. Additional information can be found in the instructions for California form FTB 3805V, Net Operating Loss (NOL) Computation and NOL and Disaster Loss Limitations – Individuals, Estates, and Trusts.

Head of Household

For taxable years beginning on or after January 1, 2015, California requires taxpayers who use head of household (HOH) filing status to file form FTB 3532, Head of Household Filing Status Schedule, to report how the HOH filing status was determined.

Financial Incentive for Turf Removal

For taxable years beginning on or after January 1, 2014, and before January 1, 2019, taxpayers can exclude from gross income any amount received as a rebate, voucher, or other financial incentive issued by a local water agency or supplier for participation in a turf removal water conservation program. Additional information can be found in the instructions for California Schedule CA (540 and 540NR).

Penalty Assessed by Professional Sports League

For taxable years beginning on or after January 1, 2014, an owner of all or part of a professional sports franchise will not be allowed a deduction for the amount of any fine or penalty paid or incurred, that was assessed or imposed by the professional sports league that includes that franchise. Additional information can be found in the instructions for California Schedule CA (540 and 540NR).

New Employment Credit

For taxable years beginning on or after January 1, 2014, and before January 1, 2021, the New Employment Credit (NEC) is available to a qualified taxpayer that hires a qualified full-time employee on or after January 1, 2014, and pays or incurs qualified wages attributable to work performed by the qualified full‑time employee in a designated census tract or economic development area, and receives a tentative credit reservation for that qualified full‑time employee. In addition, an annual certification of employment is required with respect to each qualified full-time employee hired in a previous taxable year. In order to be allowed a credit, the qualified taxpayer must have a net increase in the total number of full-time employees in California. Any credits not used in the taxable year may be carried forward up to five years. If a qualified employee is terminated within the first 36 months after beginning employment, the employer may be required to recapture previously taken credits. For more information, go to ftb.ca.gov and search for nec or get form FTB 3554, New Employment Credit.

Repeal of Geographically Targeted Economic Development Area Tax Incentives

The California legislature repealed and made changes to all of the Geographically Targeted Economic Development Area (G-TEDA) Tax Incentives. Enterprise Zones (EZ) and Local Agency Military Base Recovery Areas (LAMBRA) were repealed on January 1, 2014. The Targeted Tax Areas (TTA) and Manufacturing Enhancement Areas (MEA) both expired on December 31, 2012. For more information, go to ftb.ca.gov and search for repeal tax incentives.

California Competes Tax Credit

For taxable years beginning on and after January 1, 2014, and before January 1, 2030, the California Competes Tax Credit is available to businesses that want to come to California or stay and grow in California. Tax credit agreements will be negotiated by the Governor’s Office of Business and Economic Development (GO-Biz) and approved by the California Competes Tax Credit Committee. The California Competes Tax Credit only applies to state income or franchise tax. Taxpayers who are awarded a contract by the committee will claim the credit on their income or franchise tax returns using credit code 233. The credit can reduce tax below the tentative minimum tax. Any credits not used in the taxable year may be carried forward up to six years. For more information, go to the GO‑Biz website at business.ca.gov or ftb.ca.gov and search for ca competes or get form FTB 3531, California Competes Tax Credit.

Like-Kind Exchanges

For taxable years beginning on or after January 1, 2014, California requires taxpayers who exchange property located in California for like‑kind property located outside of California under IRC Section 1031, to file an annual information return with the FTB. For more information, get form FTB 3840, California Like‑Kind Exchanges, or go to ftb.ca.gov and search for like kind.

Cancellation of Debt Income (CODI)

For taxable years beginning on or after January 1, 2014, and before January 1, 2019, California did not conform to the federal recognition of business debt reacquisition CODI under IRC Section 108(i). If you recognized the CODI for federal tax purposes, then you must deduct the federal CODI amount. See Schedule CA (540), Part I, line 12 instructions for more information.

Net Operating Loss (NOL) Carryback

NOLs incurred in taxable years beginning on or after January 1, 2013, shall be carried back to each of the preceding two taxable years. For an NOL incurred in a taxable year beginning on or after January 1, 2015, the carryback amount shall be 100% of the NOL.

Individuals, Estates, and Trusts compute the NOL carryback in Part IV of form FTB 3805V. For more information, get form FTB 3805V.

Election to Waive Carryback

Any taxpayer entitled to a carryback period pursuant to IRC Section 172(b)(3) may elect to relinquish/waive the entire carryback period with respect to an NOL incurred in the 2018 taxable year. By making the election, the taxpayer is electing to carry an NOL forward instead of carrying it back in the previous two years.

To make the election, check the box in Part I under Section C – Election to Waive Carryback, of form FTB 3805V, and attach form FTB 3805V to the tax return. For more information, get form FTB 3805V.

Mandatory Electronic Payments

You are required to remit all your payments electronically once you make an estimate or extension payment exceeding $20,000 or you file an original tax return with a total tax liability over $80,000. Once you meet this threshold, all subsequent payments regardless of amount, tax type, or taxable year must be remitted electronically. The first payment that would trigger the mandatory e-pay requirement does not have to be made electronically. Individuals that do not send the payment electronically will be subject to a 1% noncompliance penalty.

You can request a waiver from mandatory e-pay if one or more of the following is true:

- You have not made an estimated tax or extension payment in excess of $20,000 during the current or previous taxable year.

- Your total tax liability reported for the previous taxable year did not exceed $80,000.

- The amount you paid is not representative of your total tax liability.

For more information or to obtain the waiver form, go to ftb.ca.gov/e-pay. Electronic payments can be made using Web Pay on FTB’s website, EFW as part of the e-file return, or your credit card.

Estimated Tax Payments

Taxpayers are required to pay 30% of the required annual payment for the 1st required installment, 40% of the required annual payment for the 2nd required installment, no installment is due for the 3rd required installment, and 30% of the required annual payment for the 4th required installment.

Taxpayers with a tax liability less than $500 ($250 for married/RDP filing separately) do not need to make estimated tax payments.

Backup Withholding

With certain limited exceptions, payers that are required to withhold and remit backup withholding to the Internal Revenue Service (IRS) are also required to withhold and remit to the FTB on income sourced to California. If the payee has backup withholding, the payee must contact the FTB to provide a valid taxpayer identification number, before filing the tax return. Failure to provide a valid taxpayer identification number may result in a denial of the backup withholding credit. For more information, go to ftb.ca.gov and search for backup withholding.

Registered Domestic Partners (RDP)

Under California law, RDPs must file their California income tax return using either the married/RDP filing jointly or married/RDP filing separately filing status. RDPs have the same legal benefits, protections, and responsibilities as married couples unless otherwise specified.

If you entered into a same sex legal union in another state, other than a marriage, and that union has been determined to be substantially equivalent to a California registered domestic partnership, you are required to file a California income tax return using either the married/RDP filing jointly or married/RDP filing separately filing status.

For purposes of California income tax, references to a spouse, husband, or wife also refer to a California RDP, unless otherwise specified. When we use the initials RDP they refer to both a California registered domestic “partner” and a California registered domestic “partnership,” as applicable. For more information on RDPs, get FTB Pub. 737, Tax Information for Registered Domestic Partners.

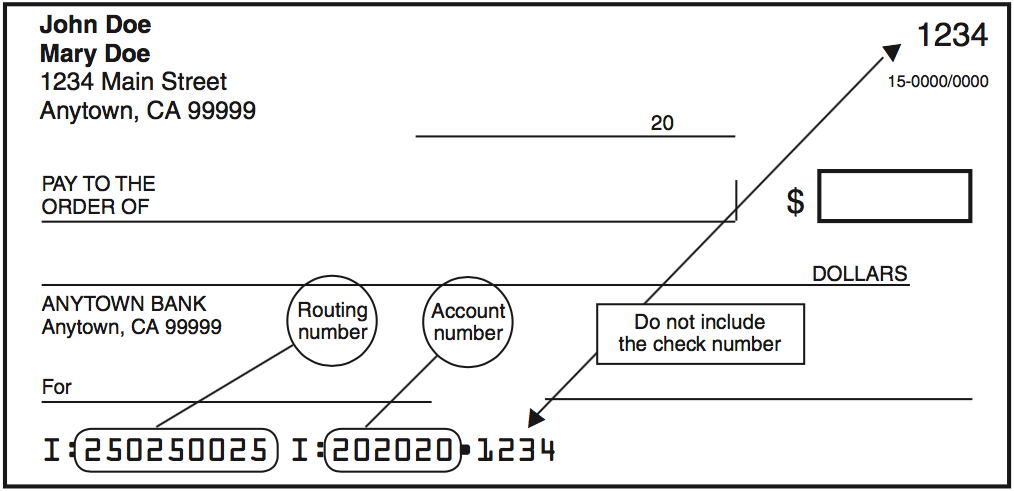

Direct Deposit Refund

You can request a direct deposit refund on your tax return whether you e-file or file a paper tax return. Be sure to fill in the routing and account numbers carefully and double-check the numbers for accuracy to avoid it being rejected by your bank.

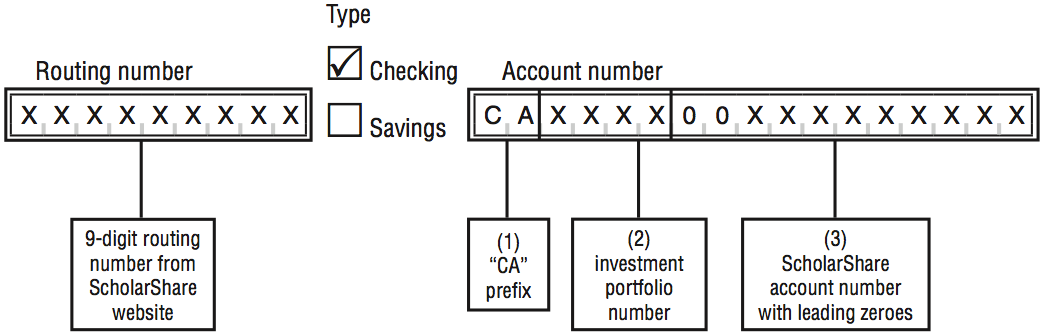

Direct Deposit for ScholarShare 529 College Savings Plans

If you have a ScholarShare 529 College Savings Plan account maintained by the ScholarShare Investment Board, you may have your refund directly deposited to your ScholarShare account.

California Disclosure Obligations

If the individual was involved in a reportable transaction, including a listed transaction, the individual may have a disclosure requirement. Attach federal Form 8886, Reportable Transaction Disclosure Statement, to the back of the California tax return along with any other supporting schedules. If this is the first time the reportable transaction is disclosed on the tax return, send a duplicate copy of the federal Form 8886 to the address below. The FTB may impose penalties if the individual fails to file federal Form 8886, or fails to provide any other required information. A material advisor is required to provide a reportable transaction number to all taxpayers and material advisors for whom the material advisor acts as a material advisor.

TAX SHELTER FILING

ATSU 398 MS F385

FRANCHISE TAX BOARD

PO BOX 1673

SACRAMENTO CA 95812-9900

For more information, go to ftb.ca.gov and search for disclosure obligation.

Which Form Should I Use?

Tip: e-file and you won’t have to decide which form to use! The software will select the correct form for you.

Were you and your spouse/RDP residents during the entire year 2018?

- Yes. Check the chart below to see which form to use.

- No. Use the Long or Short Form 540NR. To download or order the California Nonresident or Part‑Year Resident Income Tax Booklet, go to ftb.ca.gov/forms or see, “Where to Get Income Tax Forms and Publications.”

| Form 540 2EZ

Form not included in this booklet. If you qualify to use Form 540 2EZ, see “Where To Get Income Tax Forms and Publications” to download or order this form. |

Form 540 | |

|---|---|---|

| Filing Status | Single, married/RDP filing jointly, head of household, qualifying widow(er) | Any filing status |

| Dependents | 0-3 allowed | All dependents you are entitled to claim |

| Amount of Income | Total income of:

You cannot use Form 540 2EZ if you (or your spouse/RDP) can be claimed as a dependent by another taxpayer, and your TOTAL income is less than or equal to $14,551 if single; $29,152 if married/RDP filing jointly or qualifying widow(er); or $20,652 if head of household. |

Any amount of income |

| Sources of Income | Only income from:

|

All sources of income |

| Adjustments to Income | No adjustments to income | All adjustments to income |

| Standard Deduction | Allowed | Allowed |

| Itemized Deductions | No itemized deductions | All itemized deductions |

| Payments | Only withholding shown on Form(s) W-2 and 1099-R |

|

| Tax Credits |

|

All tax credits |

| Other Taxes | Only tax computed using the 540 2EZ Table | All taxes |

Tip:

If you qualify to use Form 540 2EZ, you may be eligible to use CalFile.

Visit ftb.ca.gov and search for calfile. It’s fast, easy, and free.

If you don’t qualify for CalFile, you qualify for e-file.

Go to ftb.ca.gov and search for efile options.

2018 Instructions for Form 540 — California Resident Income Tax Return

References in these instructions are to the Internal Revenue Code (IRC) as of January 1, 2015, and the California Revenue and Taxation Code (R&TC).

Before You Begin

Complete your federal income tax return Form 1040, U.S. Individual Income Tax Return, before you begin your Form 540, California Resident Income Tax Return. Use information from your federal income tax return to complete your Form 540. Complete and mail Form 540 by April 15, 2019. If unable to mail your tax return by this date, see page 2.

Tip: You may qualify for the federal earned income credit. See page 2 for more information.

Note: The lines on Form 540 are numbered with gaps in the line number sequence. For example, lines 20 through 30 do not appear on Form 540, so the line number that follows line 19 on Form 540 is line 31.

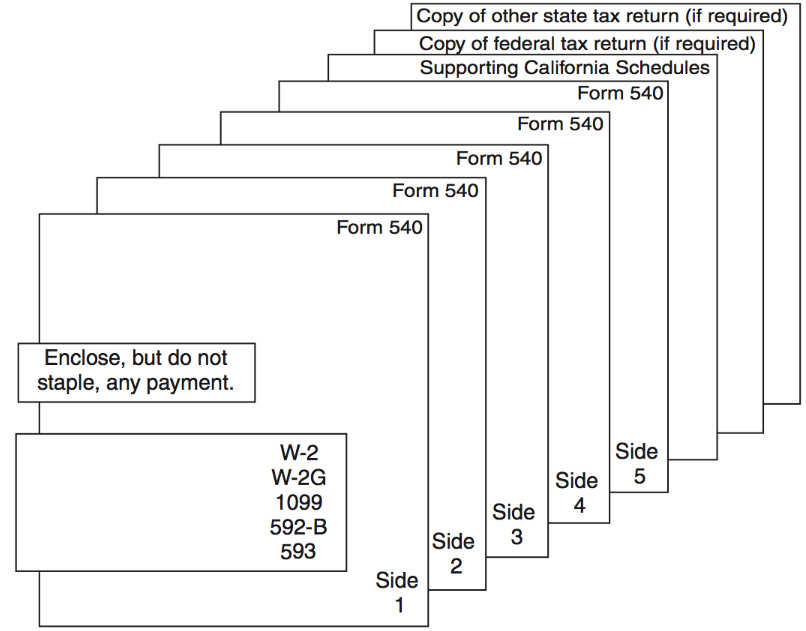

Caution: Form 540 has five sides. When filing Form 540, you must send all five sides to the Franchise Tax Board (FTB).

If you need to amend your California resident income tax return, complete an amended Form 540 and check the box at the top of Form 540 indicating AMENDED return. Attach Schedule X, California Explanation of Amended Return Changes, to the amended Form 540. For specific instructions, see “Instructions for Filing a 2018 Amended Return” on page 29.

Filling in Your Tax Return

- Use black or blue ink on the tax return you send to the FTB.

- Enter your social security number(s) or individual taxpayer identification number(s) at the top of Form 540, Side 1.

- Print numbers and CAPITAL LETTERS between the combed lines. Be sure to line up dollar amounts.

- If you do not have an entry for a line, leave it blank unless the instructions for a line specifically tell you to enter -0-. Do not enter a dash, or the word “NONE.”

Name(s) and Address

Print your first name, middle initial, last name, and street address in the spaces provided at the top of the form.

Suffix

Use the Suffix field for generational name suffixes such as “SR”, “JR”, “III”, “IV”. Do not enter academic, professional, or honorary suffixes.

Additional Information

Use the Additional Information field for “In-Care-Of” name and other supplemental address information only.

Foreign Address

If you have a foreign address, follow the country’s practice for entering the city, county, province, state, country, and postal code, as applicable, in the appropriate boxes. Do not abbreviate the country name.

Principal Business Activity (PBA) Code

For federal Schedule C (Form 1040), Profit or Loss From Business (Sole Proprietorship) business filers, enter the numeric PBA code from federal Schedule C (Form 1040), line B.

Date of Birth (DOB)

Enter your DOBs (mm/dd/yyyy) in the spaces provided. If your filing status is married/RDP filing jointly or married/RDP filing separately, enter the DOBs in the same order as the names.

Prior Name

If you or your spouse/RDP filed your 2017 tax return under a different last name, write the last name only from the 2017 tax return.

Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN)

Enter your SSN in the spaces provided. If filing a joint tax return, enter the SSNs in the same order as the names.

If you do not have an SSN because you are a nonresident or resident alien for federal tax purposes, and the Internal Revenue Service (IRS) issued you an ITIN, enter the ITIN in the space for the SSN. An ITIN is a tax processing number issued by the IRS to foreign nationals and others who have a federal tax filing requirement and do not qualify for an SSN. It is a nine-digit number that always starts with the number 9.

Filing Status

Line 1 through Line 5 – Filing Status

Check only one box for line 1 through line 5. Enter the required additional information if you checked the box on line 3 or line 5. For filing status requirements, see page 3.

Use the same filing status for California that you used for your federal income tax return.

Exception: If you file a joint tax return for federal, you may file separately for California if either spouse was:

- An active member of the United States armed forces or any auxiliary military branch during 2018.

- A nonresident for the entire year and had no income from California sources during 2018.

Caution – Community Property States: If the spouse earning the California source income is domiciled in a community property state, community income will be split equally between the spouses. Both spouses will have California source income and they will not qualify for the nonresident spouse exception.

If you had no federal filing requirement, use the same filing status for California you would have used to file a federal income tax return.

Registered domestic partners (RDPs) who file single for federal must file married/RDP filing jointly or married/RDP filing separately for California. If you are an RDP and file head of household for federal purposes, you may file head of household for California purposes only if you meet the requirements to be considered unmarried or considered not in a domestic partnership.

If you filed a joint tax return and either you or your spouse/RDP was a nonresident for 2018, you must file the Long or Short Form 540NR, California Nonresident or Part-Year Resident Income Tax Return.

Exemptions

Line 6 – Can be Claimed as Dependent

Automated Phone code: 601

Check the box on line 6 if someone else can claim you or your spouse/RDP as a dependent on their tax return, even if they chose not to.

Line 7 – Personal Exemptions

Did you check the box on line 6?

- No

- Follow the instructions on line 7.

- Yes

- Ignore the instructions on line 7. Instead, enter in the box on line 7 the amount shown below for your filing status:

- Single or married/RDP filing separately, enter -0-.

- Head of household, enter -0-.

- Married/RDP filing jointly and both you and your spouse/RDP can be claimed as dependents, enter -0-.

- Married/RDP filing jointly and only one spouse/RDP can be claimed as a dependent, enter 1.

Do not claim this credit if someone else can claim you as a dependent on their tax return.

Line 8 – Blind Exemptions

The first year you claim this exemption credit, attach a doctor’s statement to the back of Form 540 indicating you or your spouse/RDP are visually impaired. If you e-file, attach any requested forms, schedules and documents according to your software’s instructions. Visually impaired means not capable of seeing better than 20/200 while wearing glasses or contact lenses, or if your field of vision is not more than 20 degrees.

Do not claim this credit if someone else can claim you as a dependent on their tax return.

Line 9 – Senior Exemptions

If you were 65 years of age or older by December 31, 2018,* you should claim an additional exemption credit on line 9. If you are married/or an RDP, each spouse/RDP 65 years of age or older should claim an additional credit. You may contribute all or part of this credit to the California Seniors Special Fund. See “Voluntary Contribution Fund Descriptions” for more information.

*If your 65th birthday is on January 1, 2019, you are considered to be age 65 on December 31, 2018.

Do not claim this credit if someone else can claim you as a dependent on their tax return.

Line 10 – Dependent Exemptions

To claim an exemption credit for each of your dependents, you must write each dependent’s first and last name, SSN and relationship to you in the space provided. If you are claiming more than three dependents, attach a statement with the required dependent information to your tax return. Count the number of dependents listed and enter the total in the box on line 10. Multiply the number you entered by the pre-printed dollar amount and enter the result.

If your dependent child was born and died in 2018 and you do not have an SSN for the child, enter “Died” in the space provided for the SSN and include a copy of the child’s birth certificate, death certificate, or hospital records. The document must show the child was born alive. If you e-file, attach any requested forms, schedules and documents according to your software’s instructions.

Line 11 – Exemption Amount

Add line 7 through line 10 and enter the total dollar amount of all exemptions for personal, blind, senior, and dependent.

Taxable Income

Refer to your completed federal income tax return to complete this section.

Line 12 – State Wages

Automated Phone code: 204

Enter the total amount of your state wages from all states from each of your Form(s) W-2, Wage and Tax Statement. This amount appears on Form W-2, box 16.

If you received wages and do not have a Form W-2, see “Attachments to your tax return.”

Line 13 – Federal Adjusted Gross Income (AGI) from Form 1040, line 7

RDPs who file a California tax return as married/RDP filing jointly and have no RDP adjustments between federal and California, combine their individual AGIs from their federal tax returns filed with the IRS. Enter the combined AGI on line 13.

RDP adjustments include but are not limited to the following:

- Transfer of property between spouses/RDPs

- Capital loss

- Transactions between spouses/RDPs

- Sale of residence

- Dependent care assistance

- Investment interest

- Qualified residence interest acquisition loan & equity loan

- Expense depreciation property limits

- Individual Retirement Account

- Interest education loan

- Rental real estate passive loss

- Rollover of publicly traded securities gain into specialized small business investment companies

RDPs filing as married/RDP filing separately, former RDPs filing separately, and RDPs with RDP adjustments will use the California RDP Adjustments Worksheet in FTB Pub. 737, Tax Information for Registered Domestic Partners, or complete a federal pro forma Form 1040. Transfer the amount from the California RDP Adjustments Worksheet, line 37, column D, or federal pro forma Form 1040, line 7, to Form 540, line 13.

Line 14 – California Adjustments – Subtractions [from Schedule CA (540), line 37, column B]

If there are no differences between your federal and California income or deductions, do not file a Schedule CA (540), California Adjustments — Residents.

If there are differences between your federal and California income, i.e. social security, complete Schedule CA (540). Follow the instructions for Schedule CA (540). Enter on line 14 the amount from Schedule CA (540), line 37, column B. If a negative amount, see Schedule CA (540), line 37 instructions.

Line 15 – Subtotal

Subtract the amount on line 14 from the amount on line 13. Enter the result on line 15. If the amount on line 13 is less than zero, combine the amounts on line 13 and line 14 and enter the result in parentheses. For example: “(12,325).”

Line 16 – California Adjustments – Additions [from Schedule CA (540), line 37, column C]

If there are differences between your federal and California deductions, complete Schedule CA (540). Follow the instructions for Schedule CA (540). Enter on line 16 the amount from Schedule CA (540), line 37, column C. If a negative amount, see Schedule CA (540), line 37 instructions.

Line 18 – California Itemized Deductions or California Standard Deduction

Decide whether to itemize your charitable contributions, medical expenses, mortgage interest paid, taxes, etc., or take the standard deduction. Your California income tax will be less if you take the larger of:

- Your California itemized deductions.

- Your California standard deduction.

California itemized deductions may be limited based on federal AGI. To compute limitations, use Schedule CA (540). RDPs use your recalculated federal AGI to figure your itemized deductions.

On federal tax returns, individual taxpayers who claim the standard deduction are allowed an additional deduction for net disaster losses. For California, deductions for disaster losses are only allowed for those individual taxpayers who itemized their deductions.

If married/or an RDP and filing separate tax returns, you and your spouse/RDP must either both itemize your deductions (even if the itemized deductions of one spouse/RDP are less than the standard deduction) or both take the standard deduction.

If someone else can claim you as a dependent, you may claim the greater of the standard deduction or your itemized deductions. To figure your standard deduction, use the Form 540 – California Standard Deduction Worksheet for Dependents.

Itemized deductions.

Figure your California itemized deductions by completing Schedule CA (540), Part II, lines 1 through 30. Enter the result on Form 540, line 18.

If you did not itemize deductions on your federal income tax return but will itemize deductions for your Form 540, first complete federal Schedule A (Form 1040), Itemized Deductions. Then check the box on Side 2, Part II of the Schedule CA (540) and complete Part II. Attach both the federal Schedule A (Form 1040) and California Schedule CA (540) to the back of your tax return.

Standard deduction.

Find your standard deduction on the California Standard Deduction Chart for Most People. If you checked the box on Form 540, line 6, use the California Standard Deduction Worksheet for Dependents.

California Standard Deduction Chart for Most People

Do not use this chart if your parent, or someone else, can claim you (or your spouse/RDP) as a dependent on their tax return.

| Your Filing Status | Enter On Line 18 |

|---|---|

| 1 – Single | $4,401 |

| 2 – Married/RDP filing jointly | $8,802 |

| 3 – Married/RDP filing separately | $4,401 |

| 4 – Head of household | $8,802 |

| 5 – Qualifying widow(er) | $8,802 |

The California standard deduction amounts are less than the federal standard deduction amounts.

California Standard Deduction Worksheet for Dependents

Use this worksheet only if your parent, or someone else, can claim you (or your spouse/RDP) as a dependent on their return. Use whole dollars only.

- Enter your earned income from: line 2 of the “Standard Deduction Worksheet for Dependents″ in the instructions for federal Form 1040.

- Minimum standard deduction: $1,050.00.

- Enter the larger of line 1 or line 2 here.

- Enter the amount shown for your filing status:

- Single or married/RDP filing separately, enter $4,401.

- Married/RDP filing jointly, head of household, or qualifying widow(er), enter $8,802.

- Standard deduction. Enter the smaller of line 3 or line 4 here and on Form 540, line 18.

Line 19 – Taxable Income

Capital Construction Fund (CCF)

If you claim a deduction on your federal Form 1040, line 10 for the contribution made to a capital construction fund set up under the Merchant Marine Act of 1936, reduce the amount you would otherwise enter on line 19 by the amount of the deduction. Next to line 19, enter “CCF” and the amount of the deduction. For details, see federal Publication 595, Capital Construction Fund for Commercial Fishermen.

Tax

When figuring your tax, use the correct filing status and taxable income amount.

Line 31 – Tax

To figure your tax, use one of the following methods and check the matching box on line 31:

- Tax Table. If your taxable income on line 19 is $100,000 or less, use the tax table beginning on page 87. Use the correct filing status column in the tax table.

- Tax Rate Schedules. If your taxable income on line 19 is over $100,000, use the tax rate schedule for your filing status on page 93.

- FTB 3800. Generally, use form FTB 3800, Tax Computation for Certain Children with Unearned Income, to figure the tax on a separate Form 540 for your child who was 18 and under or a student under age 24 on January 1, 2019, and who had more than $2,100 of investment income. Attach form FTB 3800 to the child’s Form 540.

- FTB 3803. If, as a parent, you elect to report your child’s interest and dividend income of $10,500 or less (but not less than $1,050) on your tax return, complete form FTB 3803, Parents’ Election to Report Child’s Interest and Dividends. File a separate form FTB 3803 for each child whose income you elect to include on your Form 540. Add the amount of tax, if any, from each form FTB 3803, line 9, to the amount of your tax from the tax table or tax rate schedules and enter the result on Form 540, line 31. Attach form(s) FTB 3803 to your tax return.

To prevent possible delays in processing your tax return or refund, enter the correct tax amount on this line. To automatically figure your tax or to verify your tax calculation, use our online tax calculator. Go to ftb.ca.gov/tax-rates.

Tip: CalFile or e-file and you won’t have to do the math. Go to and search for efile.

Line 32 – Exemption Credits

Exemption credits reduce your tax. If your federal adjusted gross income (AGI) on line 13 is more than the amount shown below for your filing status, your credits will be limited.

For purposes of computing limitations based upon AGI, RDPs, recalculate their AGI using a federal pro forma or California RDP Adjustments Worksheet (located in FTB Pub. 737). If your recalculated federal AGI is more than the amount shown below for your filing status, your credits will be limited.

| If your filing status is: | Is line 13 more than: |

|---|---|

| Single or married/RDP filing separately | $194,504 |

| Married/RDP filing jointly or qualifying widow(er) | $389,013 |

| Head of household | $291,760 |

- Yes

- Complete the AGI Limitation Worksheet below.

- No

- Follow the instructions on Form 540, line 32.

AGI Limitation Worksheet

Use whole dollars only.

- Enter the amount from line 13.

- Enter the amount for your filing status on line b:

- Single or married/RDP filing separately: $194,504

- Married/RDP filing jointly or qualifying widow(er): $389,013

- Head of household: $291,760

- Subtract line b from line a.

- Divide line c by $2,500 ($1,250 if married/RDP filing separately). If the result is not a whole number, round it to the next higher whole number.

- Multiply line d by $6.

- Add the numbers from the boxes on lines 7, 8, and 9 (not the dollar amounts).

- Multiply line e by line f.

- Add the total dollar amount from lines 7, 8, and 9.

- Subtract line g from line h. If zero or less, enter -0-.

- Enter the number from the box on line 10 (not the dollar amount).

- Multiply line e by line j.

- Enter the dollar amount from line 10.

- Subtract line k from line l. If zero or less, enter -0-.

- Add line i and line m. Enter the result here and on line 32.

Line 34 – Tax from Schedule G-1 and Form FTB 5870A

If you received a qualified lump-sum distribution in 2018 and you were born before January 2, 1936, get California Schedule G-1, Tax on Lump-Sum Distributions, to figure your tax by special methods that may result in less tax. Attach Schedule G-1 to your tax return.

If you received accumulation distributions from foreign trusts or from certain domestic trusts, get form FTB 5870A, Tax on Accumulation Distribution of Trusts, to figure the additional tax. Attach form FTB 5870A to your tax return.

To get these forms, see “Order Forms and Publications.”

Special Credits and Nonrefundable Credits

A variety of California tax credits are available to reduce your tax if you qualify. To figure and claim most special credits, you must complete a separate form or schedule and attach it to your Form 540. The Credit Chart on page 25 describes the credits and provides the name, credit code, and number of the required form or schedule. Many credits are limited to a certain percentage or a certain dollar amount. In addition, the total amount you may claim for all credits is limited by tentative minimum tax (TMT); go to Box A to see if your credits are limited.

If you are not claiming any special credits go to line 40 and line 46 to see if you qualify for the nonrefundable child and dependent care expenses credit or the nonrefundable renter’s credit.

Box A

Did you complete federal Schedule C, D, E, or F and claim or receive any of the following (Note: If your business gross receipts are less than $1,000,000 from all trades or businesses, you do not have to report alternative minimum tax (AMT). For more information, see line 61 instructions.):

- Accelerated depreciation in excess of straight-line

- Intangible drilling costs

- Depletion

- Circulation expenditures

- Research and experimental expenditures

- Mining exploration/development costs

- Amortization of pollution control facilities

- Income/loss from tax shelter farm activities

- Income/loss from passive activities

- Income from long-term contracts using the percentage of completion method

- Pass-through AMT adjustment from an estate or trust reported on Schedule K-1 (541)

- Yes

- Complete Schedule P (540). See “Order Forms and Publications.”

- No

- Go to Box B.

Box B

Did you claim or receive any of the following:

- Investment interest expense. Automated Phone code: 226

- Income from incentive stock options in excess of the amount reported on your tax return. Automated Phone code: 225

- Income from installment sales of certain property

- Yes

- Complete Schedule P (540). See “Order Forms and Publications.”

- No

- Go to Box C.

Box C

| If your filing status is: | Is Form 540, line 17 more than: |

|---|---|

| Single or head of household | $268,237 |

| Married/RDP filing jointly or qualifying widow(er) | $357,650 |

| Married/RDP filing separately | $178,822 |

- Yes

- Complete Schedule P (540). See “Order Forms and Publications.”

- No

- Your credits are not limited. Go to the instructions for line 40.

Line 40 – Nonrefundable Child and Dependent Care Expenses Credit

Claim this credit if you paid someone to care for your qualifying child under the age of 13, other dependent who is physically or mentally incapable of caring for him or herself, or spouse/RDP if physically or mentally incapable of caring for him or herself. The care must be provided in California. To claim this credit, your federal AGI must be $100,000 or less and you must complete and attach form FTB 3506, Child and Dependent Care Expenses Credit, included in this booklet.

Line 43 through Line 45 – Additional Special Credits

A code identifies each credit. To claim only one or two credits, enter the credit name, code, and amount of the credit on line 43 and line 44.

To claim more than two credits, use Schedule P (540), Part III. See Schedule P (540) instructions, “How to Claim Your Credits.”

Important: Attach Schedule P (540) and any supporting schedules or statements to your Form 540.

Carryovers: If you claim a credit with carryover provisions and the amount of the credit available this year exceeds your tax, carry over any excess credit to future years until the credit is used (unless the carryover period is a fixed number of years). If you claim a credit carryover for an expired credit, use form FTB 3540, Credit Carryover and Recapture Summary, to figure the amount of the credit. Otherwise, enter the amount of the credit on Schedule P (540), Part III, and do not attach form FTB 3540.

Credit for Joint Custody Head of Household — Code 170

You may not claim this credit if you used the married/RDP filing jointly, head of household, or qualifying widow(er) filing status.

Claim the credit if unmarried and not an RDP at the end of 2018 (or if married/or an RDP, you lived apart from your spouse/RDP for all of 2018 and you used the married/RDP filing separately filing status); and if you furnished more than one-half the household expenses for your home that also served as the main home of your child, step-child, or grandchild for at least 146 days but not more than 219 days of the taxable year. If the child is married/or an RDP, you must be entitled to claim a dependent exemption credit for the child.

Also, the custody arrangement for the child must be part of a decree of dissolution or legal separation or part of a written agreement between the parents where the proceedings have been initiated, but a decree of dissolution or legal separation has not yet been issued.

Use the worksheet below to figure the Joint Custody Head of Household credit using whole dollars only.

- Enter the amount from Form 540, line 35.

- Credit percentage — 30%: × .30

- Credit amount. Multiply line 1 by line 2.

Enter the result or $469, whichever is less.

If you qualify for the Credit for Joint Custody Head of Household and the Credit for Dependent Parent, claim only one credit. Select the credit that allows the maximum benefit.

Credit for Dependent Parent — Code 173

You may not claim the Credit for Dependent Parent if you used the single, head of household, qualifying widow(er), or married/RDP filing jointly filing status.

Claim this credit only if all of the following apply:

- You were married/or an RDP at the end of 2018 and you used the married/RDP filing separately filing status.

- Your spouse/RDP was not a member of your household during the last six months of the year.

- You furnished over one-half the household expenses for your dependent mother’s or father’s home, whether or not she or he lived in your home.

To figure the amount of this credit, use the worksheet for the Credit for Joint Custody Head of Household. If you qualify for the Credit for Joint Custody Head of Household and the Credit for Dependent Parent, claim only one. Select the credit that will allow the maximum benefit.

Credit for Senior Head of Household — Code 163

You may claim this credit if you:

- Were 65 years of age or older on December 31, 2018.*

- Qualified as a head of household in 2016 or 2017 by providing a household for a qualifying individual who died during 2016 or 2017.

- Did not have AGI over $76,082 for 2018.

*If your 65th birthday is on January 1, 2019, you are considered to be age 65 on December 31, 2018.

If you meet all the conditions listed above, you do not need to qualify to use the head of household filing status for 2018 in order to claim this credit.

Use this worksheet to figure this credit using whole dollars only.

- Enter the amount from Form 540, line 19.

- Credit percentage — 2%: × .02

- Credit amount. Multiply line 1 by line 2.

Enter the result or $1,434, whichever is less.

Credit for Child Adoption Costs — Code 197

For the year in which an adoption decree or an order of adoption is entered (e.g., adoption is final), claim a credit for 50% of the cost of adopting a child who was both:

- A citizen or legal resident of the United States.

- In the custody of a California public agency or a California political subdivision.

Treat a prior unsuccessful attempt to adopt a child (even when the costs were incurred in a prior year) and a later successful adoption of a different child as one effort when computing the cost of adopting the child. Include the following costs if directly related to the adoption process:

- Fees for Department of Social Services or a licensed adoption agency.

- Medical expenses not reimbursed by insurance.

- Travel expenses for the adoptive family.

Note:

- This credit does not apply when a child is adopted from another country or another state, or was not in the custody of a California public agency or a California political subdivision.

- Any deduction for the expenses used to claim this credit must be reduced by the amount of the child adoption costs credit claimed.

Use the worksheet below to figure this credit using whole dollars only. If more than one adoption qualifies for this credit, complete a separate worksheet for each adoption. The maximum credit is limited to $2,500 per minor child.

- Enter qualifying costs for the child.

- Credit percentage — 50%: x .50

- Credit amount. Multiply line 1 by line 2.

Do not enter more than $2,500.

Your allowable credit is limited to $2,500 for 2018. Carry over the excess credit to future years until the credit is used.

Line 46 – Nonrefundable Renter’s Credit

If you paid rent for at least six months in 2018 on your principal residence located in California you may qualify to claim the nonrefundable renter’s credit which may reduce your tax. Complete the qualification record on page 22.

Line 48

Subtract the amount on line 47 from the amount on line 35. Enter the result on line 48. If the amount on line 47 is more than the amount on line 35, enter -0-.

Other Taxes

Attach the specific form or statement required for each item below.

Line 61 – Alternative Minimum Tax (AMT)

If you claim certain types of deductions, exclusions, and credits, you may owe AMT if your total income is more than:

- $95,373 married/RDP filing jointly or qualifying widow(er)

- $71,531 single or head of household

- $47,685 married/RDP filing separately

A child under age 19 or a student under age 24 may owe AMT if the sum of the amount on line 19 (taxable income) and any preference items listed on Schedule P (540) and included on the return is more than the sum of $7,600 and the child’s earned income.

AMT income does not include income, adjustments, and items of tax preference related to any trade or business of a qualified taxpayer who has gross receipts, less returns and allowances, during the taxable year of less than $1,000,000 from all trades or businesses.

Get Schedule P (540) for more information. See “Order Forms and Publications.”

Line 62 – Mental Health Services Tax

If your taxable income is more than $1,000,000, compute the Mental Health Services Tax using whole dollars only:

- Taxable income from Form 540, line 19.

- Less: $(1,000,000)

- Subtotal

- Tax rate – 1%: x .01

- Mental Health Services Tax – Multiply line 3 by line 4. Enter this amount here and on line 62.

Line 63 – Other Taxes and Credit Recapture

If you received an early distribution of a qualified retirement plan and were required to report additional tax on your federal tax return, you may also be required to report additional tax on your California tax return. Get form FTB 3805P, Additional Taxes on Qualified Plans (including IRAs) and Other Tax-Favored Accounts. If required to report additional tax, report it on line 63 and write “FTB 3805P” to the left of the amount.

California conforms to federal law for income received under IRC Section 409A on a nonqualified deferred compensation (NQDC) plan and discounted stock options and stock appreciation rights. Income received under IRC Section 409A is subject to an additional 5% tax of the amount required to be included in income plus interest. Include the additional tax, if any, on line 63. Write “NQDC” on the dotted line to the left of the amount.

If you owe interest on deferred tax from installment obligations, include the additional tax, if any, in the amount you enter on line 63. Write “IRC Section 453A interest” and the amount on the dotted line to the left of the amount on line 63.

If you used form(s):

- FTB 3540, Credit Carryover and Recapture Summary

- FTB 3554, New Employment Credit

- FTB 3805Z, Enterprise Zone Deduction and Credit Summary

- FTB 3807, Local Agency Military Base Recovery Area Deduction and Credit Summary

Include the additional tax for credit recapture, if any, on line 63. Write the form number and the amount on the dotted line to the left of the amount on line 63.

Payments

To avoid a delay in the processing of your tax return, enter the correct amounts on line 71 through line 74.

Line 71 – California Income Tax Withheld

Enter the total California income tax withheld from your:

- Form(s) W-2, Wage and Tax Statement, box 17

- Form(s) W-2G, Certain Gambling Winnings, box 15

- Form(s) 1099-DIV, Dividends and Distributions, box 15

- Form(s) 1099-INT, Interest Income, box 17

- Form(s) 1099-MISC, Miscellaneous Income, box 16

- Form(s) 1099-OID, Original Issue Discount, box 14

- Form(s) 1099-R, Distributions from Pensions, Annuities, Retirement, or Profit Sharing Plans, IRAs, Insurance Contracts, etc., box 12

Do not include city, local, or county tax withheld, tax withheld by other states, or nonconsenting nonresident (NCNR) member’s tax from Schedule K-1 (568), line 15e. Do not include withholding from Forms 592-B, Resident and Nonresident Withholding Tax Statement, or Form 593, Real Estate Withholding Tax Statement, on this line. For more details, see instructions for line 73.

Generally, tax should not be withheld on federal Form 1099-MISC. If you want to pre-pay tax on income reported on federal Form 1099-MISC, use Form 540-ES, Estimated Tax for Individuals.

Line 72 – 2018 CA Estimated Tax and Other Payments

Enter the total of any:

- California estimated tax payments you made using 2018 Form 540-ES, electronic funds withdrawal, Web Pay, or credit card.

- Overpayment from your 2017 California income tax return that you applied to your 2018 estimated tax.

- Payment you sent with form FTB 3519, Payment for Automatic Extension for Individuals.

- California estimated tax payments made on your behalf by an estate, trust, or S corporation on Schedule K-1 (541) or Schedule K-1 (100S).

Tip: To view payments made or get your current account balance, go to ftb.ca.gov and login or register for MyFTB.

If you and your spouse/RDP paid joint estimated taxes but are now filing separate income tax returns, either of you may claim the entire amount paid, or each may claim part of the joint estimated tax payments. If you want the estimated tax payments to be divided, notify the FTB before you file the tax returns so the payments can be applied to the proper account. The FTB will accept in writing, any divorce agreement (or court-ordered settlement) or a statement showing the allocation of the payments along with a notarized signature of both taxpayers.

Send statements to:

Joint Estimated Credit Allocation MS F283

Taxpayer Services Center

Franchise Tax Board

PO Box 942840

Sacramento, CA 94240-0040

If you or your spouse/RDP made separate estimated tax payments, but are now filing a joint income tax return, add the amounts you each paid. Attach a statement to the front of Form 540 explaining that payments were made under both SSNs. If you e-file, attach any requested forms, schedules and according to your software’s instructions.

You do not have to make estimated tax payments if you are a nonresident or new resident of California in 2019 and did not have a California tax liability in 2018.

Line 73 – Withholding (Form 592-B and/or 593)

Enter the total of California withholding from Form 592-B and Form 593. Attach a copy of Form(s) 592-B and 593 to the lower front of Form 540, Side 1.

If your filing status changed after escrow closed and before filing your California tax return, please contact us at 888-792-4900, prior to filing your California tax return, for instructions on how to claim your withholding credit.

Caution: Do not include withholding from federal Form(s) W-2, W-2G, or 1099, or NCNR member’s tax from Schedule K-1 (568), line 15e on this line.

Line 74 – Excess California SDI (or VPDI) Withheld

You may claim a credit for excess State Disability Insurance (SDI) or Voluntary Plan Disability Insurance (VPDI) if you meet all of the following conditions:

- You had two or more California employers during 2018.

- You received more than $114,967 in gross wages from California sources.

- The amounts of SDI (or VPDI) withheld appear on your Form(s) W-2. Be sure to attach your Form(s) W-2 to the lower front of your Form 540.

If SDI (or VPDI) was withheld from your wages by a single employer, at more than 1.00% of your gross wages, you may not claim excess SDI (or VPDI) on your Form 540. Contact the employer for a refund.

To determine the amount to enter on line 74, complete the Excess SDI (or VPDI) Worksheet below. If married/RDP filing jointly, figure the amount of excess SDI (or VPDI) separately for each spouse/RDP.

Excess SDI (or VPDI) Worksheet

Use whole dollars only.

Follow the instructions below to figure the amount of excess SDI to enter on Form 540, line 74. If you are married/RDP and file a joint return, you must figure the amount of excess SDI (or VPDI) separately for each spouse/RDP.

| You | Your Spouse/RDP | |

|---|---|---|

| 1. Add amounts of SDI (or VPDI) withheld shown on your Forms W-2. Enter the total here. | ||

| 2. 2018 SDI (or VPDI) limit | $1,149.67 | $1,149.67 |

| 3. Excess SDI (or VPDI) withheld. Subtract line 2 from line 1. Enter the results here. Combine the amounts on line 3 and enter the total, in whole dollars only on line 74.

If zero or less, enter -0- on line 74. |

Line 75 – Earned Income Tax Credit (EITC)

Enter your Earned Income Tax Credit from form FTB 3514, California Earned Income Tax Credit.

Line 76

For the Claim of Right credit, follow the reporting instructions in Schedule CA (540), Part II, line 16 under the Claim of Right.

Claim of Right: If you are claiming the tax credit on your California tax return, include the amount of the credit in the total for this line. Write in “IRC 1341” and the amount of the credit to the left of the amount column.

To determine if you are entitled to this credit, refer to your prior year California Form 540, Form 540NR (Long or Short), or Schedule CA (540 or 540NR) to verify the amount was included in your CA taxable income. If the amount repaid under a “Claim of Right” was not originally taxed by California, you are not entitled to claim the credit.

Use Tax

Line 91 – Use Tax.

You are required to enter a number on this line. If the amount due is zero, you must check the applicable box to indicate that you either owe no use tax, or you paid your use tax obligation directly to the California Department of Tax and Fee Administration.

You may owe use tax if you make purchases from out-of-state retailers (for example, purchases made by telephone, online, by mail, or in person) where California sales or use tax was not paid and you use those items in California.